Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Worldwide Exchange CNBC December 19, 2012 4:00am-6:00am EST

4:00 am

welcome to "worldwide exchange." i'm kelly evans, these are your headlines from around the world. ubs admits to fraud, paying a fine for rigging libor rates and warning it could book a loss in the fourth quarter. house republicans look to bring a plan b up for a vote in case budget talks with the white house fail. the gop's fallback to avoid the fiscal cliff is still expected to fail in the senate. and japan's nikkei 225 reaches the 10,000 mark for the first time in eight months. stocks rally after a widening trade deficit softens the yen and heightens expectations for more stimulus. we are expecting to get the latest results from germany's survey any second now. in the meantime, i can can bring you news. for example, on industrial

4:01 am

orders and sales in italy, orders flat on the month, down .2 on the month for sales and down nearly 5% on the year. so confirming some of the weakness that we know we've seen previously in the italian economy. meanwhile, another gauge perhaps for the euro as we look to the strength of it lately. that's the current counselor plus which in october was an adjusted 3.9 billion euros, up quite a bit from the 2.5 billion reported for september. now that also comes after -- a day after the european union's report suggesting that in fact the european union would have to run a surplus, given its poor demographics over the next couple of years. now let's get a quick preview of the news. for that we head to patricia, awaiting the results. what do we expect to see? >> reporter: we're expecting the second consecutive month to the upside for the business sentiment next year in germany. november was a surprise after six months to the downside. we expect december to book in a little increase again, but

4:02 am

important is here, not only the expectation part of the index but also that we get a little more oomph as to say from the current conditions. and that is going to be the big part of the numbers. we are just starting to see it. business climate index in december is out, and it rises. here we have business climate index 102.4 in december versus an expectation of 102. slightly better unanimous expected. here the current conditions, 107.7. the consensus was 1.8. that is slightly lower than expectations when it comes with the current conditions. here the expectation side of the index is 97.9. reuters was pointing to 96.2, so better than expected. there is no revisions made to november. so we do have a rise for the second consecutive month for the business sentiment index.

4:03 am

in germany what you see is a reaction from the euro. we've been trading actually fairly strong all morning. 1.30 to 2.47. it was 1.32 42 before the numbers hit the wires. we have quite a bit of support for the euro because of the s.a.p. upgrade on greece and the situation over there. we'll see also the way the market is reacting. let's have a quick look at what the dax is doing. it's been perky, up 0.15%. trading toward the 7,665 level. >> patricia, this comes at a time when people have been focusing on the strength of the euro. as we're over the 1.32 level you mentioned, certainly member countries would like to see a weaker currency. but as long as the surveys hold consistent with strength in the german economy, we're not likely to see that weakening. >> no. absolutely. and the more we get over the entire question will the euro break up or not, as long as that

4:04 am

happens we will have some more support in the euro which is not bad if you think about the quantitative easing we've seen in the eurozone and also inflation. that could be the counterpart of the equation, that we still have money being pumped into the economies wheroe ouausterity is going on. we have a little pullback possibly going forward when it comes to the euro. then again, if you look at the year of 2012, we have to put it in perspective. the euro/u.s. dollar didn't move that much whatsoever. from that point of view, i don't think that we just have to look at today or the last two days of development in euro/u.s. dollar. of course, global trade is really important for the german economy. it continues to be very important. even from a private consumption point of view, we did have quite a bit of support as of late. also because of the wages. and looking at the world bank report, also looking at the asian economies in 2013, 2014, them seeing a little better picture is very good for the

4:05 am

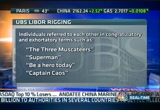

german economy and not to speak about the turnaround in the u.s. which seems to be stabilizing, looking this also at the housing market. so business sentiment better than expected. it is rising. the current conditions a little weaker than expected. add to that the financial analyst numbers we had as of late, also better than expected. not too bad. >> patricia, we'll see you again next hour. thank you very much for following all the latest there. >> sure. now, shares in ubs have edged up in early trade after the bank announced a major settlement with u.s., u.k., and swiss regulators over its role in the libor fixing scandal. with more we'll look at the story with carolyn roth with us on set. i guess we're expecting a settlement, expecting something big. what have we learned today? >> well, first of all, i mean, the market reaction -- ubs up by 1%, can you believe that? what barclays was hit with $450 million fine, i mean, we saw a big hit in barclays' share price. this fine is three time the

4:06 am

amount that barclays was fined. $1.5 billion or $1.4 billion swiss>>frank: francs. this is on the libor manipulation charges. ubs must pay swiss regulators $59 million in profits because the regulator can't fine ubs. the fine from the fsa is the biggest ever, 160 million pounds, $1.2 billion will go to the u.s. regulators. so the second biggest fine that was ever handed to a financial institution. of course, following that $1.9 billion fine that was given to hsbc. what we do know is that the company is admitting criminal wrongdoing in its japanese arm because, you know, around 30 traders worldwide had manipulated the yen libor between 2005 and 2010. the ceo speaking this morning says, you know, despite the

4:07 am

troubles in the japanese arm, he does not believe that there's -- the bank is going to be shutting down the operations in that country entirely. saying that 30 to 40 people have already left the bank. they also gave us a bit more information on what kind of impact this will have on profits. they see a fourth quarter net loss of around 2.5 billion swig franks. a full-year profit of 2.5 to 3 billion. and the most important part, why shares are trading up. they still expect a fourth quarter net new money being positive. and again, i mean, it's puzzling to some. on the other hand, investors are clearly focusing on the rebound story much more than the lobbyer story because, you know, these are things of the past. >> and also it's the "wall street journal" reporting rbs may be the next bank. we have two down but probably several more to come. it was comments -- i've got the report from the fsa, a 40-page

4:08 am

document. some of the comments that are getting focus, i think we can show a few. it's extraordinary. and again, coming after some of the things we heard from barclays. perhaps even more egregious. one trader saying to a broker -- you can read, "you keep 6s unchanged today. i will [ bleep ] do one humongous deal with you like a 50,000 buck deal, whatever. i need you to keep it as low as possible. if you do, that i'll pay you, you know, $50,000, $100,000. whatever you want. i'm a man of my word." more commentary that illustrate over time a level -- this was an institutional practice. it wasn't a one off trade here that's being focused on. >> no. >> this was something going on for quite sometime. >> it was done over a number of years. it wasn't just ubs. i know ubs may have been a central role. you know, they may have been, you know -- the bank that actually started manipulating even though we don't know that. but that's the thinking. but it's an industry matter. not just specific to ubs. >> we'll have plenty more on

4:09 am

this. dirk becker will join us next hour. thank you very much. really appreciate it. carolyn will be going back to cover the story out of the homeland soon. mean meantime, news from porsche now. i'll see if i can bring it up correctly, that is. we're still showing -- german prosecutor has issued charges against former porsche executives. if we get more details on this story, we will bring it to you. charging them with market manipulation. plenty of charges to go around this morning, for sure. if you have any thoughts this morning, want to respond to thing you've heard on the program, you know how to reach us. e-mail worldwide@cnbc.com. we'll check markets. first to asia and singapore and the details. hi. >> reporter: hey. prim good session here. still optimism that a deal will be reached over the ploifiscal f

4:10 am

stateside. domestic factors in place starting with japan. this is the real star of asia. for the last month or so the nikkei 225, shattering the 10,000 level, up 2.4%. the jen weak against the dollar -- yen is weak again the dollar which is behind the gains. more than 116% in the last five weeks. all eyes and pressure is on the boj governor. they began their policy meeting today. expectations are very high for some very aggressive monetary stimulus tomorrow. so if traders don't get what they want, we could see some disappointing action in this market. already way in overbought territory. moving to the greater chinese markets, a volatile session once again. the shanghai caught changing directions a number of times throughout the session. ending just on the flat line at 21.62. the property plays were dragging this index down. they've been some of the best performers year to date. however, we've been getting more

4:11 am

rhetoric from policymakers saying that the curbs and restrictions that have been in place for more than two years now are going to be there to stay. this is following some signs of a revival in that market. of course, as you guys know, the government has its eye and wants to cool home prices and really deflate that bubble. the hang seng managed its first winning session so far this week. up .6%, bringing it close to a 17-month high. and oil plays were big winners. we had the s&p asx 200 in australia, gains. the bsc sensex trading half a percent. back to you. >> thank you very much. a key session in japan overnight. as we pivot our focus to europe, you see stocks addi adding .3%. consistent with the rally we've seen over the last several trading sessions and apparently having plenty to do with the possible resolution of u.s. fiscal talks. we'll have more in a little bit. the survey also helping to lift sentiment or keep it buoyant.

4:12 am

look at the major borses. green in the harder hit regions. ftse mib, spain up better than 1%. consistent with the rally we saw yesterday. remarkable. the xetra dax adding .1%. for its part, up to close to 30% this year. the ftse 100 adding .3. the bond space, we'll look at that and talk later about the big trades that have helped some hedge funds, for example, when it comes to greek debt. for the time being, mario's comments this summer is have techively kept the bond gleelds a tight range since then six months or so now, this is going. and differentiation across the space where italy price rising, not the case for spain which is seeing its yield up to 5.3. and i know we haven't mentioned this in a while, but i want to draw your attention here. the ten-year gild in the u.k., 1.957%. extraordinary. we're not off the 2% market in

4:13 am

the spread, widening significantly. coming up on the program today, the count is set to get underway in south korea following general elections. we'll head to seoul to find out whether the country could elect its first female leader. the bank of england releases minutes from its latest policy meeting. what could the vote on quantitative easing mean for the gild market? and good news and bad for bilibong. we'll ask if they can regain the market's trust. then fedex reports before the bell in the u.s. will the strong holiday season help offset the impact of sluggish growth in the u.s. economy and global economy?

4:16 am

welcome back to the program. over in south korea the polls have just closed. according to the latest figures, voter turnout was above 70%, far exceeding the numbers in the presidential elections in 2007 and 2002. this result could also see the country get its first female leader. we have more on this report from seoul. >> reporter: south koreans went it the polls today with two

4:17 am

choices ahead of them. the daughter of a former dictator and the ruling party candidate. and the left-leaning democratic united party's candidate, a protege of the former president who is still remembered as a symbol of democratic reforms. but rather than a choice for the future, many say this battle is shaping up to be a thing of the past. this ad paid for by her party depict a scar on her face which they say shows her determination to overcome adversity. others say it shows she's scarred by her father's legacy. he rose to power in the '60s and was credited with kick starting korea's economy. he's also blamed for committing human rights abuse during his time in office. >> in the eyes of koreans, a mixed legacy. economic low very, very positive. in terms of democracy, the developments of korean democracy

4:18 am

quite negative. so he does have this -- there's this sort of love him more hate him thing. >> reporter: standing in contrast is the opposition leader. last week's abrupt departure of rival candidate and software mogul has given moon's popularity a boost among young voters. he also has an impressive political pedigree, serving as chief of staff under the former president. like his ex-boss, portrays himself as a man of the people. it's a delicate issue that the south korean president bak has tried to bridge but with little luck. he's been more successful in handling the economic response to global financial crisis. the challenges remain. >> translator: in the short term, the incoming government has to recover growth which has been sluggish lately. also, debt is a problem, but more importantly, facility investments by companies must be

4:19 am

reunited in order to lift the domestic economy and create jobs. >> reporter: south korea's neighbor to the north are going to require a great deal of skill for whichever candidate wins the election. but to most it's still a battle of legacies, not policies, where ironically swing voters and the younger generation are likely to dictate the outcome. >> and speaking of the outcome, we're getting a few exit polls reported by dow jones and reuters out of south korea. polls did just close. reuters citing south korean tv says the exit polls show park, the female conservative candidate, winning with a vote of 50.1%. no surprise. dow jones, meanwhile, saying the exit polls are divided. the polling at least now would suggest an extremely narrow win. as we get more update on the figures, we'll bring them to you and keep an eye on the broader market reaction but more likely it will be focused on what happens when markets reopen tomorrow. south korea was closed for

4:20 am

trading today. now the u.s. has slapped duties on wind turbine towers on china on price its says were unfairly cheap. this comes as washington welcomes a high-level chinese delegation led by the vice premier. his team is in the u.s. to talk trade and economy. he's expected to meet with u.s. treasury secretary tim geithner tomorrow. wang is the first official from the new leadership team to visit with the u.s. for more on the impact and implications of this, let's speak with frank ching, adjunct associate professor at the chinese university of hong kong. frank, hi. the first news that we're getting out of this appears to be more import duties s. this going to be the theme of u.s./china relations, or do you expect these meetings to be more of a thaw? >> well, i think that these are the first meetings since the new leadership in china was installed. and since president obama saw -- well, won second term.

4:21 am

i think both sides want to make use of this occasion to improve their relationship. so this joint annual meeting is a platform, and i think that they will probably be able to achieve some progress on issues of concern to both sides. but i don't see any sweeping changes. >> what's interesting, frank, and you point this out, are comments we got out of china's commerce minister or commerce secretary suggesting concern about quantitative easing because it was lowering the value of the foreign reserves, the dollar reserves that china holds. so china's apparently looking to sort of diversify away from those reserves into more generating assets. but it's having difficulty doing so because the u.s., because a lot of nations have been reluctant to let them in. any sign that attitudes there may be starting to change, particularly in light of the candidate deal? >> yeah. i think the nexen deal was good for china.

4:22 am

the prime minister made in t clear this is not the beginning of a new trend. he said this is the end of a trend. and that the canadian government has been withdrawing from ownership of resources and different parts of economy, and it's not about to hand thing over to foreign governments. the thing is most of these chinese companies trying to invest are state-owned corporations. therefore, they represent the chinese government. and do not necessarily operate on purely market principles. this is something that not only canada is wary of, but the united states also. the -- there is concern that the national security might be involved. you might remember that back in 205, the same commission company tried to buy unical in the united states and encountered extensive opposition from the u.s. congress. and they had to withdraw. and then after that, china tried

4:23 am

to buy something in australia. and encountered opposition. i think that there is a suspicion of chinese intentions whenever they try to buy into areas that are sensitive. and the chinese minister of commerce yesterday showed a statement saying that this is protectionism, and it's discriminatory. >> and frank, how should we read the statement? is it a stepping up of the kind of rhetoric we've seen in the past? is it any kind of read-through to how the next administration is going to handle the u.s./china relationship? >> well, i think that it's a little too early to tell that this is symptomatic of the new administration. but i do expect that there will be progress in certain areas. china has been asking the u.s. to lift restrictions on high-tech exports. and i gather that the obama administration is consider something kind of overhaul of the current restrictions. so there might be some change there was benefit to china. and on the u.s. side, the u.s. would like china to lift

4:24 am

restrictions on imports of livestock. and it looks like china is willing to do that on a gradual basis. so i think that there would be some positives coming out of these meetings today and tomorrow. >> and lastly, frank, what would be the most significant policy move period to come from this. again, aside from the news we've already heard about the import duties, are you looking for any big-name tie-ups, or is this about meeting and shaking hands, especially because the u.s. leadership still isn't settled, erkts speci especially for next year? >> i think there is agreement on negotiating and investment treaty, that that would be sort of a signal of a breakthrough, that the two sides are willing to sit down and talk about this. an investment treaty may be able to overcome a lot of the obstacles that both sides see in the other country. and on the u.s. side, not just the u.s. but on the western side, there's a feeling that the chinese market is not open and

4:25 am

that open markets should be a two-way street. it's not just the west is open, china has to be open, too. >> we'll leave it there. adjunct associate professor at the chinese university of hong kong. frank, thank you very much. now for more on this topic, in fact on asia more bradley, let's get more on the conversation. global head of economics at society national. when we look into 2013, how -- how he been of power shifting, and is china going to start using its foreign reserves as more of a bargaining tool? >> well, i don't really think they will. and i think what's important to see is that the foreign exchange reserves are also part of the currency policy. if china were to massively diversify their foreign exchange reserves special different currencies, then they would also have to change the currency policy. so the two really to my mind go hand in hand. now, that doesn't necessarily mean that if they're buying u.s.

4:26 am

assets that it has to be u.s. treasuries. but it does have to be u.s. dollars. so in that respect, if there are discussions around investment treaties, these kind of developments could be quite interesting because perhaps you could have some diversification in terms of the asset mix per se. and that would be -- that would be an something development. but you know, keep in mind that in the course of the past 12 months, china hasn't really been that important a buyer of u.s. treasuries. and i think that's the other thing that we have to remember is that there is an interesting link. now whether it's spurious or whether it's -- whether it's a real link, we have noticed an something lynch between expansion of the fed's balance sheet and increases in china's foreign exchange reserves. that may be power issious, we have to be careful about that. remember that in 2012 it was more about operation twist. so not so much balance sheet expansion. 2013 we do expect to see significant expansion. there may be new dynamics coming in there.

4:27 am

>> we want to pick up on that in a bit. first, your food news. canadian police arrested three people overn connection with the multimillion-dollar heist of, yes, maple syrup. over $20 million worth of maple syrup was stolen from canada's strategic reserves in quebec last summer. what got our attention as we're talking about reserves is the fact that canada has strategic reserves of maple syrup. we want to know what your country is holding reserves of. is it marmite, olive oil in italy? in the u.s. what would it be, ketchup perhaps? we'll get more on these important matters. we want to know, again, what you would suggest. e-mail thoughts to worldwide@cnbc.com. the fed's policy meeting will be out. live reaction when we come back. i always wait until the last minute. can i still ship a gift in time for christmas?

4:28 am

yeah, sure you can. great. where's your gift? uh... whew. [ male announcer ] break from the holiday stress. ship fedex express ber 22nd for christmas delivery.

4:30 am

you're watching "worldwide exchange." stocks rising in europe on the back of a second straight increase in business sentiment. the etho institute suggests corporate confidence is improving as the eurozone crisis abates. ubs admits to fraud, agreeing to pay a $1.5 billion

4:31 am

fine for rigging libor rates and warns of a loss in the fourth quarter. house republicans plan a plan b in case talks fail. the gop's suggested fiscal cliff is expected to fail in the senate. and stocks rally after a widening trade deficit softens the yen and hietdeeightens expectations for more monetary stimulus. and as promised, minutes from the bank of england's december meeting are out. they show that the monetary policy committee voted 9-0 to hold the rate at 0.5%. 8-1 to hold the quantitative easing program steady at 375 billion pounds. david miles,the descenter the ee

4:32 am

dissenter there. they talk about the rise in sterling since mid 2011 unwelcome saying it may be inconsistent with global rebalancing. and they're calling britain's lost competitiveness a potential headwind to growth. we're pleased to be joined by jeffrey dix, chief u.k. economist at novus capital markets. your reaction? >> if i could pick up about the point on the exchange rate, that's exactly what mervyn king said at the november inflation report press conference, that the rise in sterling was unwelcome. this is a bank which has missed its nation target consistently for -- its inflation target consistently for five years. yesterday's numbers tell us they're going to miss the fourth quarter number for this year. they're already too low. if they were serious about inflation, they would welcome an appreciation in the exchange rate because it would reduce imported inflation, and imported inflation from oil and commodities is what's pushing up inflation in the u.k. >> i suppose the point being, though, if you look over the last couple of years, sterling's been rising, so have food and

4:33 am

oil prices. so they really haven't gotten much of the benefit. the hope i guess being that maybe going forward they would. >> no, but they're saying that they would like sterling to be weaker. the only logical conclusion is that they're pretty indifferent to inflation. and they're far more concerned with the real economy and particularly with rebalancing demand. the governor's told us repeatedly that that's vital and necessary for the u.k. over the medium term. and they would much rather look at the real economy. i describe this as constrained discretion. they are constrained ultimately by the inflation target. but month by month they have complete discretion over what they do, and month by month they ignore the inflation target. >> and i wonder if they're more focused, if policymakers are more focused on the exchange rate than inflation, as you suggest. is that warranted? is the exchange rate something they should be using and trying to weaken? is there a point at which they start to do so? >> i'm not necessarily saying

4:34 am

that the bank of england is wrong to do what they're doing. all i'm saying is that they are ignoring their inflation target and have repeatedly done so. of course the depreciation that we've seen in sterling over the last five years is welcome and will ultimately help rebalance our economy or boost exports and hold back imports. of course there's no sign of it doing that at the moment which suggests there thereare struck supply payments, as well. we would like and welcome a weaker exchange rate. but it doesn't help at all on the inflation problem. >> what happens from here? what does the bank of england do? mark carney's coming in. do you expect a major change in their stance? do you expect a continued focus on perhaps using quantitative easing as a way of getting that exchange rate down? >> well, from what i've been saying already, you might gather that i think that even if they were given an entirely different target, it wouldn't make a difference at all. they could have been asked to

4:35 am

target putting a man on the moon the last five years, and they would have still done exactly what they have done month by month. so give them a target for nominal gdp. give them an inflation target. and it comes back to constrained discretion. they'll be constrained to say that they are trying to hit that target. but month by month, they will have the discretion to ignore it. >> what that suggests is actually not to expect any major change under mark carney because what they've effectively been doing is kind of what greg yip called the other day a nominal gdp targeteding light. they're basically -- targeting light. they're basically using outpudge gauges to figure out monetary policy regardless of inflation. if he says to scrap the inflation rate, you're saying they basically have already? >> i don't think he can say that. it's the chancellor's decision. i think in the next six months, he'll probably walk into exactly the situation we have today. in six months' time, we'll probably still be voting 8-1 for quantitative easing. i don't think anything's going to change. and then it's up it him to try and persuade the chancellor to change the target.

4:36 am

but as he's said, he's not minded to do so. >> last point, we've seen the employment side look better lately. do you actually expect the size of the bank of england's balance sheet to grow over the next five months? >> i wouldn't say so. the employment numbers as you say are remarkable given what's going on in the real economy. and that's why i think policy's pretty well on hold. >> we'll leave it there. jeffrey dix, chief u.k. economist at novus capital markets. we'll see how the bank of england feels about putting a man on the moon. germany's etho business index has climbed for the second month in december, coming ahead of a reuter's poll. economists attribute the gains to a calming eurozone crisis which they said was helping firms regain trust in growth prospects. we have more from global head of economics at societe generale. the etho survey comes in as expected, maybe a little stronger. is it a good sign or does it mean that the ecb will have a hard time, say, lowering interest rates in order to support the economy? >> i think there are a couple of

4:37 am

things to pick up on here. first of all, a stronger etho, yes, good news. any growth we can get in europe is good news. the fact that germany is seeing stronger growth doesn't necessarily resolve on the european periphery. and i think this is really important to understand this divergence that we've seen in europe for a very long time now with the periphery and recession and germany doing better. and this is where perhaps we see a little bit of a paradox in the european situation. the ecb has fixed funding coming in with the omt as an insurance backing up the esm. at the same time, to access that program, to have that insurance, countries have to sign up to a program of austerity and structural reform. the same time we know that austerity and structural reform puts in danger the growth, risks social tension -- >> negative cycle, right -- >> of course to see downgrades in those countries. we see it's a very difficult situation in europe today. now coming back to the ecb and the ques of rate cut, i

4:38 am

would say that if the ecb were to cut rates, it wouldn't really make a material change to my economic outlook. what would make a material change to my economic outlook is if we were able to address the financial fragmentation that we see within europe today. >> this is what's so interesting. actually what mario draggy has done is removed the impetus for the fragmentation. bond yields are stabilizing in the periphery. you're not necessarily seeing the impulse for, say, fiscal union that you might have seen six months ago. >> well, i think what we have seen is that the big quantum leaps we've had in the crisis have been under market pressure. that doesn't necessarily mean we want to experiment too much on extreme market pressure either. i think the actions from the ecb we have to consider welcome. but what we also need consider is if we look within europe today is how can we get the cost of funding down for countries in the periphery. and perhaps if the ecb are thinking about new measures,

4:39 am

taking some inspiration from the bank of england, looking at things like the funding for lending scheme could be ideas. having said that, we haven't seen much impact in the u.k. from those measures yet. >> no, we haven't. >> it borrows down to the confidence on europe. and i think that's still going to be a long way in rebuilding. >> in a word, your likelihood that greece leaves the eurozone at this point? >> i think the long distanikeli remains low. i also think the likelihood of greek public finances, that this is the final package on greece, will also be very low. >> extremely low. they seem to be part and parcel, don't they? mikayla will stay with us. we want to check on markets quickly and give a sense of the trade we're seeing so far. green arrows across the board pretty much. whether spurred by optimism, deserved we should say on, fiscal cliff talks in the u.s. or not remains to be seen. the ftse at session highs just about there. up about half a percent. similar rallies especially for the ibex, trying to finish off on a stronger note.

4:40 am

and we show what's happening, more differentiation there. yields in spain and italy are lower whereas we were seeing spanish yield a little higher earlier in the session. 5.3 and 4.4% for spain and italy on the ten year respectively, extraordinary. and again, focused on the gild this morning. we are amazingly close to the level and close to the gap with the bund. the europe solar doll/dollar ai finishing at 84.31 -- 1.32. after a string of reports the last couple of days that included stronger than expected -- not stronger than expected but a relatively firm cpi report. dollar solar yen, 84.32, adding and supporting the rally we saw in the nikkei. sticking with japan, disappointing trade figures gave investors hope the boj will have little choice but to ease monetary policy.

4:41 am

we have more from the nikkei, live from tokyo. >> reporter: hi, kelly. japan's trade deficit widened the most in ten months in november. last month japan recorded an 11.4 billion dollar trade gap after exports dropped 4% on the strong yen and weak global demand. shipments to china slipped 14.5% hurt by the mainland's growth pullback and anti-japan sentiments there which muted the demand for japanese goods. there were bright spots. car exports to the u.s. grew which meant that in november japanese trade to the -- japan's trade to the u.s. was bigger than trade to china. still, the overall weak numbers play into the hand of incoming prime minister ibe. he is likely to push the fwoj stimulate growth. the central bank will announce its latest policy decision tomorrow. back to you. >> okay. thank you very much for that. now samsung electronics has decided to quit its lawsuit aimed at halting the sale of

4:42 am

apple's products in europe. this decision comes just one day after the south korean tech giant scored a victory in one of its patent battles with apple in a california courtroom. samsung said it dropped its injunctions in europe in the interests of consumer choice. it did not specifically say it would abandon its court battle for compensation. samsung electronics flat there, but -- sorry, korean markets were closed today for the presidential election. apple adding 2.9% yesterday. no wonder the nasdaq was doing so well. weak sales at home and abroad forcing some of asia's top retailers to slash earnings forecasts and consider takeover bids. we have more on the story. hi, dee. >> reporter: hey, that's right. some brands that are in decline. we had two companies really slumping today in trade. the brands in question are espirit and billabong, once seen as valuable names that consumers would income to. they are now in decline.

4:43 am

espirit is of course a europe-focused retailer, and billabong synonymous with surf wear. falling 7% in hong kong today, though ended down 4.5% in hong kong after issuing a profit warning which sparked downgrades for morgan stanley and jpmorgan. late last year, espirit launched a four-year turnaround plan to basically revive its brand in the company. but it's struggled it compete in europe where it competes with brand such as h&m and zara, owned by inditex. in argue -- in august it hired a former inditex second to turn it around. in australia, shares slumped more than 13% today. and its future is being questioned. now it did receive a takeover offer today worth some $556 million u.s. half a billion dollars, however, there's been some discussion over whether or not billabong would actually accept this offer. and its shares did plunge because it gave a profit warning

4:44 am

outlook saying that it's actually giving tries speculation that the latest -- rise to speculation that the latest offer shows due diligence, period. you may not believe it, but the company has actually rejected several offers before this. one of them worth as much as $900,000. so it has been a pretty slow but amazing fall from grace for both of these retailers. >> reporting from singapore, keeping an eye on the fashion trends. thanks. here's the agenda on ashe tomorrow. in japan the central bank will announce its latest policy decision. the yen and nikkei have been such a focus leading up to that. in india, parliament wraps up its almost month-long winter session. and in the u.s., house republicans say they expect to pass their own tax bill as a backup plan to avoid the fiscal cliff. nbc news reports this measure, which is being called plan b, will likely go to a vote on thursday. the measure would extend the bush-era tax cuts for everyone making less than $1 million a year. it's not expected to get through the democratic-controlled

4:45 am

senate, and the white house has already dismissed the plan. so we asked mikayla, still with us, what progress the markets seem to be seeing here, and are they wrong? >> well, this is a discussion that's ongoing. and i think we're going to continue to see that debate rolling. our expectation is to see a temporary extension similar to what we had last year before the end of this year, and then actually only reach a final agreement early next year. but we do expect the two parties to come together and reach that agreement early next year. and that i think and the key point is that once that uncertainty from the cliff is removed, that really will help the u.s. economy. we've done some work on the policy uncertainty in the u.s., looking at just how much of a drag that's been on the economy. we estimate that it may have cost over two million jobs and as much as 2.5% points of gdp. as we look ahead, coming into the beginning of next year, getting that uncertainty removed, there will be a drag

4:46 am

from the fiscal tightening. we see a drag of just over one point of gdp. at the same time, the lifting of that uncertainty should actually pave the way for a much better outlook for the u.s. economy heading into the second half of the year and especially into 2014. while we look for almost 3% growth. >> 3% growth. now -- what's interesting is whether the u.s. -- where the u.s. then falls kind of when we look at the world and people trying to figure out investment options, do they keep capital at home, look for better opportunities abroad. if you're saying that we've shaved 2.5% points on gdp from uncertain uncertainty, it would suggest the fundamental growth rate is strong by historical standards. >> well, think about the large output gap that we still have. it's been one of the slowest on record. there's potential for the u.s. economy to recover. and we do expect that that sustainable recovery could come through starting in the second half of the year, heading into 2014. when it comes to investment

4:47 am

decisions, there's of course the fundamentals of the economy. they look good in the u.s. it also seems a favorable environment for the u.s. dollar given forecasts. we have to consider the relative evaluations. i would urge investors to look at that in making their decisions. >> and real quick, fitch here saying if the u.s. goes over the cliff into recession, it could lose its aaa rating. does that matter? >> i don't think that there will be a big reallocation away from u.s. treasuries if the u.s. loses its rating. what will matter much more, though, is that if we go over the cliff, it will create a tremendous uncertainty shock. and talking about the price tag of that uncertainty. now our expectation is if we do go over the cliff, that there will actually be legislation put in place to reverse some of that coming in further down 2013. the initial start to the year will be very, very painful. both in terms of market uncertainty and in terms of the impact on the real economy. so it would be a real negative. a drowngrade would probably be the -- downgrade would probably

4:48 am

be the least of my concerns in context. >> a year of two halves. global head of economics at societe generale. appreciate it. straight ahead, find out just how well or not well my attempt at cooking a traditional holiday meal went. mom and dad, i'm sorry. we'll be right back.

4:51 am

welcome back to the program. some news to bring you. about 2013 when we look at key events, this is sure to be one of them, the esm. a european stability mechanism. the permanent bailout fund that will replace the temporary essf will sell the first bond in the first half of 2013. t-bill sales from the esm will replace sales from the esff. those auctions to begin in january. the efsf is planning to raise between $55 billion and $60 billion worth of long-term debt in 2013. so the debt issuance will start at least from the esm side in the t-bill. it will be t-bills in nature that will start earlier in the year. now the european bailout funds together will finance the

4:52 am

rollover of two bills in the amount of almost nine billion euros in 2013. these headlines from reuters and dow jones, point being this will be one to watch in january. in the meantime, the wet summer in the u.k. could ruffle consumer feathers this festive season. turkey prices in britain are up around 4% on the year, while vegetables will have you digging deeper in your pocket. brussels sprouts prices have shot up 24%. potatoes for roasting are 43% more expensive. remarkable. and speaking of christmas dinner, i went to the st. paul's branch of latalia de chef to find out about international expansion plans. while i was there, i did get a little help learning how to make a christmas dinner of my own. >> so what we're going do next, we're going to prepare the duck breast. so we've got some fat to remove, some since uew to remove. >> are we removing it by hand? >> of course. that's what the knife if for. ♪ >> executive chef andre dupont

4:53 am

at the city of london branch has promised it teach even a kitchen novice like me how to make the perfect holiday meal. this is the second london location of the french company, but plenty more are in the pipeline. >> we plan it open four more in the next tweerks all o years, a london. >> why is the u.k. so ripe for expanding a cooking school business? blame the likes of tv chefs. >> the desire to learn about cooking, to watch cooking is everywhere. it's ubiquitous across the media. you watch any tv program at night, you've got cooking there. any magazine, newspaper, you've got cooking there. we've become very used to cooking. we're a nation of armchair chefs. >> how did my attempt at making holiday dinner go? okay, i'm going try to get a little of everything. so good. it's worth the effort to actually make something like this for my family.

4:54 am

that would be great. >> absolutely. >> wow. turns out with a little classically trained french help, even i can make christmas dinner. from the kitchens of latalia de chefs, i'm kelly evans. if there's hope for me, there's hope for anybody. the real trick will be replicating the recipes. they are available the company's web site if you want to look them up. they were delicious, although i'm distraught about the fact that brussels sprouts are more expensive now. canadian police arrested three people overnight in connection with a multimillion dollar heist of maple syrup. over $20 million of maple syrup was stolen from canada's, yes, strategic reserves in quebec last summer. we were amazed to hear about the strategic reserves. and if canada can hold strategic reserves of maple syrup, what would your country hold reserves of? would it be marmite, olive oil, ketchup? e-mail us, worldwide@cnbc.com. tweet us here @@cnbcwex.

4:55 am

going, going gone. depleting resources isn't just a concern for environmentalists but for the community, their. as finite materials become scarer and prices inch upwards, some companies have to look at alternatives. the resource crunch may be around the corner. joining us for more is tom delay, chief executive of the carbon trust. tom, welcome. >> good morning. >> you've been trying to draw attention to this issue. how do we know beyond this general sense of resource depletion just how unprepared companies are for this transition? >> well, we advise governments and businesses around the world, particularly leading organizations on resource efficiency and carbon reduction. we wanted to see whether there was a broader passion here and whether other organizations were engaged in the same way as leading organizations. we did market research. we looked into almost 500

4:56 am

executive opinions on essentially resource efficiency, resource crunch, what they were doing -- >> what do you mean resource? what kind of resources are we talking about? the resources are broad. you look at energy, water, you look at land use, minerals, in particular valuable minerals. you look at how those impact on businesses, and whether businesses are actually anticipating the resource crunch coming down the track. what we found looking right around the world, we looked at research in the u.k. and the u.s., in brazil, korea, and in china. businesses are generally not prepared for the resource crunch. they are basically saying, look, when it comes along, it's going to increases prices. it's going to limit our ability to scale our business geographic -- >> can you blame them? how do you prepare for something you can't exactly quantify? >> i think they can prepare. and they can prepare right now. they're looking ahead and saying it's going to cost us. they see it as a cost, not an opportunity. therefore, they're saying, well, we're not going to deal withdrawal it -- they're looking six, ten years out in some cases. yet they're laying down the products, services and supply chains, their businesses will

4:57 am

depend on in 10 and 15 years. they're doing that right now. we know that if you build in resource efficiency into your plans now, in 10, 15 years times you'll be more efficient. >> places in london are building green roofs, but over time it pays for itself. >> absolutely. typically there's an up-front cost but not necessarily a big one. to do something more efficiently is simply building efficiency and effectiveness into your supply chain, your business. builds resilience in. less than half of the companies we spoke to actually assess the risk to do with resource depletion. that's extraordinary when you look at how many businesses across the central spread actually are very dependent on resources for their core business. >> this is one area where britain has been a leader. you note there's plenty more detail in the report. thank you for coming by. >> a pleasure. straight ahead on the program, u.s. lawmakers are racing to strike a deal on the fiscal cliff before santa comes to town. but will they be able to reach a

4:58 am

deal, or tell be a compromise? i always wait until the last minute. can i still ship a gift in time for christmas? yeah, sure you can. great. where's your gift? uh... whew. [ male announcer ] break from the holiday stress. ship fedex express ecember 22nd for christmas delivery.

5:00 am

welcome back to "worldwide exchange." i'm kelly evans. these are your headlines from around the world. house republicans plan to bring up a plan b in case talks collapse.

5:01 am

but agreements in the senate are expected to fall. ubs agrees to pay a $1.5 billion fine for rigging libor rates and warns it could book a loss in the fourth quarter. stocks rise in europe on the backs of a second week of business sentiment. corporate confidence is improving as the eurozone crisis abates. and japan's nikkei breaches the 10,000 mark for the first time in more than eight months. stocks rally after a widening trade deficit softens the yen and heightens expectations for more stimulus. now stocks in the u.s. rallied yesterday on hopes for a resolution of the fiscal cliff. but in the meantime, we haven't gotten one today. doesn't seem to be stopping the mood. markets looking to rally again. the dow industrial average pointed higher by about 25 points. remarkably the dow i believe, yes, less than 6% away from its

5:02 am

all-time nominal high in october of 2011. the nasdaq, s&p also pointed higher. the nasdaq was the outperformer yesterday, up 1.5%. apple up almost double that. take a look at what's happening in the trading session across europe and the world. the cnbc ftse global 300 shows we're up .3%. it's been green arrows across the board. european markets for the most part higher led by spain's ibex. up 1.5%. the ftse mib adding .7% in italy. the xetra dax, outperformer of the year, adding .3%. we mentioned that business sentiment in germany held firm, helping to support sentiment. the ftse 100 up more than .5% as it edges closer to the 6,000 levels. the bank of england showed there was david miles pushing for more quantitative easing in december. the rest voting to hold the program steady. we'll look into next year and see what the new leadership will look like. i want to look in particular at the gild.

5:03 am

ten year yielding 1 p.110%. and italy and spain seeing yields coming down. italy below 4.4%. you know, when it comes to the urgency with regard to italy or, say, spain asking for help, you can understand why policymakers are reluctant and probably will be until their hand is forced. spain below 5.4%. the euro dollar is stronger as is sterling. euro/dollar adding .3%. nearly 133. remarkable if you consider all that we've been through. perhaps a headwind again for the periphery that would prefer to see a lower exchange rate. meantime, also the dollar/yen one to focus on, adding about -- just about .2%, just under.2% today, 84.35 the level there. for more on what the weaker yen has been doing to support trade in the nikkei and across asia, let's get to deirdre wang morris, joining us from

5:04 am

singapore. hi. >> reporter: hey, kelly. that weaker yen has been doing a lot to continue to fuel the rally that we are seeing in japanese equities. now another thing that it's doing is heaping pressure on the governor there. they began their two-day policy meeting today. and expectations are very high tomorrow that they will come out with some aggressive monetary easing. for now, the real fear among investors is that they might miss out in the japanese equity rally. a lot have been getting in. look at this -- pretty remarkable. 2.4% jump on top of gains of about 15% in the last five weeks. okay, the greater chinese markets, though, struggled today. particularly the shanghai composite. in and out of positive and negative territory to end flat. we did get more rhetoric from policymakers that capital markets would be further opened up to foreign investors. however, it's the domestic retail investors that haven't really bought into this rally yet. still cautious ahead of the end

5:05 am

of the year. and do keep in mind that the shanghai comp is one of the worst performing markets in the region. still under water by about 2% for the year. the hang seng, however, pulling off its first winning session of the week, up .6%. no thanks to espirit, the clothing retailer that kelly and i were talking about earlier. lowering its guidance. so it was down by about 5%. however, providing some support in hong kong, we did have the big energy majors. and this is after beijing said that it would -- it was going to let market forces play more of a role in determining energy prices. the s&p asx 200 in australia. we saw nice gains to the tune of half a percent on fiscal cliff optimism. that was really a theme across all of these markets today. so the s&p asx gaining half a percent. it was miners and bankers that led the rally. no thanks to billabong, another retailer on the decline. getting a bid, a takeover bid for more than half a billion u.s. dollars. however, lowering its earnings guidance.

5:06 am

and we have the sensex in india still trading for another half-hour. currently seeing gains of about half a percent. this after their policy decision yesterday. kelly, back to you. >> deirdre, thank you very much for that. business sentiment in germany has climbed for the second straight month in december. coming in just ahead of a reuter poll, and patricia sarvis now with details on the survey. hi, and how is this being taken over there? hi there, very positively indeed. i think at the moment we are trading at session highs again after the index. perhaps you can see behind me we had a leg up right after the efo index -- ifo index came through. the euro/u.s. dollar reacting positively, 132.77. i looked at that. that should be more or less session high. overall, this has been taken positively indeed. the details here especially with regards to the commons from the chief economist interest. first of all,y in further cuts seen from the -- no further cuts seen from the ecb as far as

5:07 am

they're concerned at the institute. gdp for the fourth quarter should book in a fall of 0.3%. however, turnaround back to growth in the first quarter of 2,013. -- first quarter of 2013. we did expect this weaker picture in the last quarter of 2012 for germany. interesting also, the different segments in terms of performance. we had a little weakness coming through from wholesale and retail. very good development, though, on manufacturing, as well as construction. now what is driving the index higher the second consecutive month is the expectation index. remember, if you look at the actual businesses, while they're still feeling more positive, are they putting their money where their mouth is? that's a question mark. as far as analysts are concerned that i speak to on the ground, they actually really want to see the current conditions constantly improving for them to really start seeing the businesses putting money and investing, putting in the capex into the economy.

5:08 am

trying to turn around in a more long-term -- this economy to growth. all in all, i think the number is pointing to a stabilization, especially at the beginning of 2013 for the german economy. we heard from the world bank, also looking at asia upgrading there. the growth forecast. we've seen as of late that the u.s. is not looking that bad. i.e., if you look at car numbers there, especially porsche aone of the biggest luxury items you can get, having had a fantastic november. expecting a fantastic year 2012 should be the lead also for 2013. >> thank you very much for that. we'll turn to the u.s. to see what's on the agenda today. see if we can disrupt the rally that's started. as we mentioned, november housing starts are out at 8:30 a.m. eastern. they're expected to drop by 3% to an annualized rate of 865,000. of course building permits are expected to rise 1% in this gauge of future building. on the earnings front, look for results before the open from general mills and fedex which we will be previewing shortly. after the close, we'll hear from

5:09 am

accenture and bed, bath, and beyond. here's a look at the other top stories -- oracle second-quarter profits rose 18%, revenues 3%, beating forecasts on strong sales of new software. revenue growth was held down by the company's hardware business which declined more than expected. but oracle says it was business as usual during the quarter, despite uncertainty by customers over the fiscal cliff. cfo software cat says customers want to close deals and there's been generally no negative impact on pricing. oracle shares responding positively in the after-hours session. in frankfurt trade, adding 2.4%. knight capital has agreed to be bought by rival market getgo by $3.75 a share or $2 billion. getco beat out virtue financial after it sweet noted the offer to make it 2/3 cash. dwight's ceo tom joyce will step down but remain on as chairman. he'll be replaced by getco's

5:10 am

daniel coleman. knight nearly went bankrupt in august after a software glitch flooded them with trades. getco is part of the investment group that helped risk the firm. knight adding better than 8% this morning. of course, they've been hammered over the last six months. the u.s. justice department has reached a settlement with publishing giant penguin group or allegations that it conspired with rivals to hike prices for ebooks. in april, the government sued claiming apple and several publishers worked to push prices above the 999 level that amazon was charging to download books for its kindle. that trail was set to begin in june or is set to begin next june i should say. penguin is owned by pearson. we can look at how pearson is trading except we don't have a share price. moving on, mark zurichburg is donating $500 million in facebook stock to a philanthropic and investment group. on a facebook page, he says he and his wife have signed a giving pledge, an effort launched by bill gates and

5:11 am

warren buffett a few years back. involves a promise to give away at least half of one's fortune during his or her lifetime. zurichburg has already don't -- zuckerburg has already donated to the middle school system in newark, new jersey. and ubs has agreed to settle over its role in the libor scandal. so can the swiss bank now finally rehabilitate its image and its business? analysis when we come back. [ male announcer ] this december, remember -- what starts with adding a friend... ♪ ...could end with adding a close friend. the lexus december to remember sales event is on. this is the pursuit of perfection. i always wait until the last minute.

5:12 am

can i still ship a gift in time for christmas? yeah, sure you can. great. where's your gift? uh... whew. [ male announcer ] break from the holiday stress. ship fedex express by december 22nd for christmas delivery.

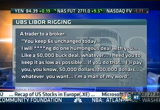

5:14 am

you are watching "worldwide exchange." these are your headlines -- republicans offer a backup plan to avoid the fiscal cliff as washington races to seal a deal before christmas. ubs agrees to fork over a $1.5 billion fine over libor fraud. japan's nikkei tops 10,000 for the first time since april on hope for more monetary easing. and it's going to be one of the most closely watched events of 2013. the italian elections, that is. today something indications. italy's prime minister, mario monti, has postponed his end of the year press conference. dow jones reporting that delay may signal a possible delay in the budget vote. now this budget vote, of course, being the key hurdle he wanted to get through before resigning. he announced his intention to resign in the last couple of days. that clearing the way for a potential return to politics of

5:15 am

silvio berlusconi. again, not clear exactly why the post there has -- there's been a postponement of the end of the year press conference. that is the case as we are learning this morning. moving on to shares in ubs which are at the top of the smi in zurich after the bank announced a settlement with u.s., u.k., and swiss regulators over its role in the libor fixing scandal. ubs will pay a total fine of $1.5 billion after admitting to manipulating the rate. as well as pleading guilty to charges of fraud and bribing brokers. the swiss bank says the fine will lead to a greater than expected fourth quarter loss. but that it will not need to raise new capital. carolyn, the response here by shares positive leading, in fact, the borce as we see it. >> ubs is the better performer on the smi, up by 2.3%. yes, the story, you know, has leaked over the last couple of days. we thought the loss would be bigger. maybe -- or the fine, rather, would be about $1.6 billion.

5:16 am

now it's only $1.5 billion. still, this is a very, very hefty fine. i mean, it's three times the amount that barclays was fined over the summer, $450 million the amount then. and it does suggest that ubs played a much bigger role than initially thought. >> and what's interesting, we can show quickly a couple of the comments that are coming out of this report from the fsa indicating this wasn't just a one-off case. there was quite a lot going on, and they were flagrant with dealing with one another. >> absolutely. it was systematic. this was libor manipulation, not just the yen libor, but all ranges of libor around the world. for a period of five to six to seven years. and ubs says that 30, 40 traders left the bank over this. again, ubs is going to be posting bigger than expected loss for the fourth quarter, 2.5 billion swiss franc thes there. will we see outflows as a result of this?

5:17 am

and it's -- its big wealth management unit, probably not. >> an interesting question. let's bring in dirk becker, head of banking sector research at capital markets and covers ubs. dirk, how does this news change your view on the company if at all? >> no, it doesn't change my view on the company. i had a pretty negative view on the whole story for quite a while now. this view has not really been reflected in the markets. i think what we're seeing is the building of a bubble of expectations which discounted by investors now which -- ubs can't really deliver on, i think, next year. >> carolyn talked a little about the potential for reputational damage or fallout with regards to clients. do you expect anything like that? the reaction markets today would certainly suggest that the fallout here will be contained. >> yeah. it is -- they already announced that the q4 flows have been in

5:18 am

management. they had inflows of 30, 40 billion swiss francs. the interest rates now are more like dolores 3 billion to $4 billion. the flows have come down significantly. and i think most of the inflows are coming from markets which are remote like in asia and -- and in the u.s. where maybe the reputation is not so much in damage ads it is in europe and switzerland in particular. >> definitely. dirk, i think it's fascinating. when we saw barclays being slapped this massive fine over the summer, saw this major witch-hunt going on in the u.k. so so far, and i've basebaeen following the swiss press, there's no major calls for mr. monti to step down. of course, they weren't necessarily with the bank when all this manipulation happened. someone's going to take responsibility, right? >> yeah. i think this would be really harsh on the -- on the top management. the top management is only in charge since 2011.

5:19 am

so clearly after the libor manipulation is over and -- i think we'll see something like 35 traders being charged for this, and i think this is probably what will happen. the management of the investment bank has changed several times since then. and i don't think anything would be necessary right now with the new management. >> dirk, you mentioned, too, broader concern. what happened at barclays spurred basically a restructuring. ubs we're seeing that restructuring take place. what are the prospects for this company going into 2013? >> well, ubs by its own admission expects mid single digit roes for 2013 and 2014. so this is one of the lowest roes in the banking sectorment at t -- sector. they're trading at multiples. i think we're seeing restructuring. i think there will be more litigation. we've seen that i think france is preparing litigation on the possible tax evasion charges.

5:20 am

so i think the bad news for ubs is not over. >> we'll leave it there. dirk becker is head of financials, head of banking sector research capital markets. thank you very much for your time. carolyn, a real pleasure, as well. a good day to have you on set. >> absolutely. absolutely. >> but we'll follow, of course, the fallout from ubs shares as we watch financials open in the u.s. stick around. ahead, o the program, oracle beats the street with second quarter results. and as it expands even more into cloud computing, we'll find out if the sky's the limit for the softwaremaker. stay tuned.

5:23 am

the s&p 500 has been up for eight of the last ten sessions. will today make it 9-11? that's the case with the implied open. up four points as we speak. the dow industrial average looking to add 40 points at the open. it is less than 6% from its record nominal high reached back in october of 2007. the nasdaq, for its part, has added nearly 3% in the last two trading sessions alone. up 17% this year. powered by apple and also oracle. its second quarter profits rose 18%, and revenues 3% beating forecasts on strong sales of new software. revenue growth was held down by the company's hardware business. oracle says it was business as usual during the quarter despite uncertainty over the fiscal

5:24 am

cliff. company cfo says his clients have continued to spend, customers want to close deals, and there's been no negative impact on pricing. so for more we're joined by daniel i've, senior analyst at fbr capital markets from new york. good morning. strong set of numbers from oracle. what's the read through for the rest of the market? >> it's a great read-through, especially for q4. a lot of nervousness out there. they came through with strong numbers, and it bodes well for overall technology going into 2013. >> want to look at the details here. particularly the hardware versus software shift. now, oracle, of course, the software business continues to did well. hardware, they bought sun microsystems for, what, $5 billion, $5.6 billion a couple of years ago. and that division has posted a drop in revenue every quarter since. are we to believe that they'll finally show growth here come march? >> a good question.

5:25 am

look, the software, you know, at this point, that's the meat and potatoes. a new software license up 10% organically. you looked real strong. that's the focus for investors. the hardware continues to be a work in progress. again, they're focusing on the more profitable areas. the key is they still expect that to grow by the end of the year. that's when most investors are focused on it. it's a smaller piece. obviously, you know, a higher profitable area. and i think they've done a good job sort of getting rid of the nonprofitable areas of sun. >> and software being as strong as it is, is one sector i guess where the question becomes sustainability. do we see after a 17% quarter those kinds of double digit figures continuing, and do they need to continue? >> i think to some extent they need to continue in terms of you need to see better license performance from oracle. and you saw it this quarter. you know, i think if you leak at the move to the cloud, that's really going to be, you know,

5:26 am

kind of front and center. and they're going to be a key driver to fuel that double digit growth on the license performance. and there's a lot of fuel left in the oracle engine. and i think they got the right products, the right time especially on the cloud side. and on the application side. and really feels like it's coming together. going into 2013. >> how much of this is already priced in, and, you know, what's oracle going to have to do now because it has seen shares rally. >> sure. i mean, the stocks acted very well. you know this year, i think investors, you know, have caught up to some of the optimism. but again, i think, you know, if they're successful in cloud and some market share gains there, and that hardware business starts to turn around, i think there's a lot of upside here. i think you can look at a high third-hour stock, especially on the large cap front. a secular story with upside like that where they're positioned, it's -- you know, a good position to be for investors that are focused on oracle.

5:27 am

>> real quick, does this mean acquisitions? >> look, i mean, they're going to continue to do acquisitions. obviously they've been pretty aggressive over the last few years. i'd expect smaller deals. again, i think there's going to be continued focus on the cloud, and this is a company where, you know, their crystal ball, they've done a good job kind of skating toward where the puck's going. and i think on the cloud side is where they expect more acquisitions. and it's hard to argue with their success over the last few years. >> okay. hockey analogy which we'll take on this chilly morning. senior analyst at fbr capital markets. daniel, thanks. ahead on "worldwide exchange," hedging your bets. it's been a mixed year for the hedge fund industry. we'll get the outlook for 2013, see if recovery is in sight.

5:30 am

in headlines, house republicans plan to bring up a plan b in case talks collapse. the gop's fallback it avoid the sfloifl still expected to fail in the senate. ubs admits to fraud, agreeing to pay a $1.5 billion fine for rigging libor rates,

5:31 am

warns it could book a loss in the fourth quarter. stocks are higher in europe on the back of a second straight increase in german business sentiment. the ifo incent report corporate confidence is improving as the crisis abates. and japan's nikkei breaches the 10,000 mark for the first time in more than eight months. a wider trade deficit softens the yen and heightens expectations for more stimulus. u.s. futures are looking to build on the rally that we've seen take shape over the last couple of weeks. the dow as i mentioned earlier up eight of the last ten sessions, poised to add 35 point at the open. the nasdaq added nearly 3% in the last two trading sessions. the s&p 500 looking to add about three or four points at the open. also less than 10% away from its nominal highs. the ftse global 300 gives you a sense. overnight we've seen shares

5:32 am

rally nearly .4% at this point. the positive mood in sabasia ha cued to the european session. the bank showed willing tons extend quantitative easing. the cac koran adding half a percent, and here up 1.5%. how do you make money in the markets? today shouldn't be hard. here's what experts have been telling us all morning -- >> i think u.s. is starting good into next year. if we start to see the you are cross not be on the front page every single day, think the you are will continue it push forward. maybe it's coming to sort of an end. the market may be getting bored with it. i think sterling will be a focus. >> credit for telecom italia telefonica, low duration rates have been with short duration high yield.

5:33 am

long loans. loans over high yield. you have to have high yield, i prefer to have loans. and continue to take advantage of technicals. there's a lot of cash in the market. i think it's going to keep credit. >> i do think investors need to be careful ton get too ahead of themselves on the equities. at some point we either need to see the copper price moving higher, as you allude, to or potentially the copper equities starting to come down. well, maybe he consulted the oracle at delphi. reports say dan lobe, the hedge fund manager who runs third point, has made a $500 million profit after betting greece wouldn't be forced it leave the eurozone. third point tend dered the bulk of the $1 billion position in greek bonds built up a few months ago as part of a buyback deal by athens monday. lobe is one of a handful of hedge fund gurus to enjoy big returns this year. broadly speaking, it's been a disappointing year for the industry. for more, peter larell i joins

5:34 am

us, v.p. at e-vestment. telling us generally how hedge funds have done this year and what 2013 could look like. >> sure. across the hedge fund space, we've seen -- we've seen strong performance from credit-related strategies. we've seen slight underperformance, possibly disappointing performance from the equity-focus funds. emerging market strategies have performed well with china being the loan exception. and we've seen, you know, somewhat underperformance from the kmdity. if x. macro space during the year. >> yeah, i think one index showed hedge funds generally speaking up 5% this year. if you consider that the nasdaq is up 17%, you know, why are you paying two and 20? >> well, you'd have it look at where you're investing in the hedge fund space. if you look at going back to credit funds which have received the majority of inflows during the year, the funds are up around 10% with -- you know,

5:35 am

nowhere near the volatility we've seen in equity markets. even within the credit space, looking at areas like structured credit and funds investing in mortgage-backed securities. they returned almost, you know, over 18% this year on average. >> do you think that next year or going forward the fundraising, the moves that we're seeing, the investment positions will gravitate toward those industries? would that suggest that existing funds are just going to change tactics, or does that mean we'll see, you know, ones reallocated? that is, more shutting down, more capacity coming out of the industry and maybe more opportunity going elsewhere? >> well, at investment we're in a position where we can see there is pent-up demand for allocations into the hedge fund space. and looking back on 2012, we've seen that, you know, at least in the equity space investors were rewarded for accepting a certain level of -- higher level of risk. so i think two things. one, we will likely continue to see flows going to the credit

5:36 am

space. performance has warranted that, and i expect it's going to continue going forward. also in terms of investors being rewarded for accepting risk, i think we'll see flows return to the equity space. throughout 2012, we saw massive amount of -- of capital come out of equity-focused funds. i think upwards of $20 billion. so i think, you know, with the pent-up demand for the hedge fund, for hedge fund exposure, we'll start to see money come back into the equity space. but also continuing to flow to the credit space. >> yeah. i wonder, do you think we'll look back on 2007 as a once in a lifetime opportunity or moment for the industry? or do you think that if after enough years perhaps it will get back to that kind of trading environmen environment? >> you know, that's a difficult call. i think there is a certain limit to its capacity. but you know, in certain spaces, i don't think it's quite been met yet.

5:37 am

in 2007, it was a, you know -- an interesting time. and obviously assets we saw peak in mid 2008. and i think we'll regain that peak in assets, but tell happen this year or not. you know, we'll see. but there is demand for hedge fund exposure. we're seeing that from our clients. >> and lastly, i was going ask who is looking to invest into hedge funds. i imagine with pension funds underwater and in this low rate environment in particular, that's actually despite under performance by funds pushing them toward maybe some places that can offer at least the chance for better returns and hoping that that will help them, you know, when it comes to just staying above water. >> absolutely. i saw an interview last week from the adviser to a large state pension plan. she indicated that they operate under the assumption of returning 7% a year to meet their operational needs. and if you look across the hedge fund space, where you can get -- you know, at least in 2012,

5:38 am

where you could earn that 7% with any sort of -- any sort of certainty, it goes back to the credit space. about 67% of funds operating in that -- in those markets returned greater than 7% this year. and within that, you look at the mortgage space. i think it was about 91% of those funds returned greater than 7%. if you look elsewhere across the hedge fund industry, equity funds only 45% have met that kind of 7% return. emerging markets, actually 51% of those funds have returned better than 7% in 2012. at least through november. >> well, that tells you quite a bit about it. we'll see if they can keep up at least in the credit space the kinds of returns we've seen to justify those flows. peter lorelli, v.p. at e-investment. thank you very much this morning. some hopeful signs maybe for the hedge fund industry this. let's look at today's other top stories. house republicans say they expect to pass their own tax bill as a backup plan to avoid the fiscal cliff. nbc reports the measure which is

5:39 am

being called plan b will likely go to a vote on thursday. the measure would extend the bush-era tax cuts for everyone making less than $1 million a year. it's not expected to get through the democratic-controlled senate. and the white house has already dismissed the plan. plan b could offer house speaker john boehner and the gop some cover as they are -- they could argue they did what they could to stop the full impact of the fiscal cliff. oracle's second quarter profits rose 18%. and revenues were up 3%, topping forecasts on strong sales of new software. revenue growth was held down by the company's hardware business, which did decline more than expected. oracle says it was business as usual during the quarter, though, despite uncertainty by customers over the fiscal cliff. the company's ceo says clients have continued to spend this month. they want to close deals, and there's been no negative impact to pricing. oracle shares responding up in frankfurt trade by 2.4% to the upside. the federal trade commission had been expected to wrap up its antitrust probe into google's search practices this week.

5:40 am

reports say the agency will delay its decision for several weeks. and the ftc's move comes after european regulators took a hard line on google in a similar investigation. google's been accused of giving rivals lower ranking in search results which makes it harder for customers to find them. that's put pressure on google shares. they are well under performing in market, down .7% this morning. and coming up, we will take a peek into pimco's crystal ball to find out one of the world's largest fund managers thinks is in store for markets in europe for 2013. [ male announcer ] with wells fargo advisors envision planning process, it's easy to follow the progress you're making toward all your financial goals. a quick glance, and you can see if you're on track. when the conversation turns to knowing where you stand, turn to us. wells fargo advisors.

5:42 am

can i still ship a gift in time for christmas? yeah, sure you can. great. where's your gift?

5:43 am